Abstract

We provide an alternative explanation for the previous finding of analysts’ overreaction to extreme good news in earnings. We show that such finding could be a result of analysts’ rational behavior in the face of high earnings uncertainty rather than their cognitive bias. Extreme earnings performance tends to be associated with higher earnings uncertainty that generally leads to more forecast optimism. Once this effect is accounted for, the univariate result of analysts’ overreaction to extreme good news in earnings is subsumed, leaving only their underreaction in general.

Similar content being viewed by others

Notes

One may also interpret this result as analysts’ overreaction in the sense that they overestimate the mean reversion of earnings changes and forecast too high (low) following bad (good) news. It is not our point to argue over the labeling of underreaction or overreaction. We follow the Abarbanell and Bernard (1992) definition of under-/overreaction throughout the paper.

An exception is Machuga et al. (2002) who find that analyst forecast errors are negatively correlated with past economic value added.

Lim (2001) examines variables such as firm size, analyst following and poor performance and attributes their effect on forecast bias to earnings uncertainty. Although these variables are correlated with earnings uncertainty, forecast dispersion is a more direct measure of uncertainty itself. We also consider many of the variables in Lim (2001) and find that they have their own effects after forecast dispersion is controlled for, possibly for reasons other than earnings uncertainty. Moreover, a major point of our paper is that earnings uncertainty is higher for both poor and superior performance rather than only for poor performance as in Lim (2001).

We also use an alternative earnings levels measure, i.e., the most recent realized earnings EPS t−1, and discuss the results in additional analysis. Both Ali et al. (1992) and Butler and Saraoglu (1999) examine simple categories such as losses. We allow continuous changes in earnings levels and find that forecast errors behave differently within different segments of earnings levels. Some other studies use ex post realized earnings EPS t as the earnings levels measure, which is subject to a look-ahead bias (e.g., Eames and Glover 2003).

Using prior annual rather than quarterly earnings to measure MNMD produces qualitatively similar results but significantly reduces the number of available observations.

Other ways of identifying outliers, such as winsorizing or deleting a certain percentage of extreme observations, require the knowledge of the overall cross-sectional distribution that may not yet be available. We follow the 100% cutoff point rule in Eastwood and Nutt (1999) but do not remove observations with forecast errors greater than 100% using ex post earnings realizations. We only use ex ante information so that any forecast inefficiency is identifiable and improvable when the forecasts are made.

Brown (2001) documents a strong increasing trend in median forecast errors possibly because he uses a different data source (IBES), examines the single most recent quarterly forecasts rather than consensus annual forecasts, and measures forecast errors in dollar terms rather than percentages.

The number of observations in 1999 is smaller because 1999 was a partial year when the data were made available to us.

If we use the larger sample only with FE t and F t available, the slope for the upper quartile is negative and significant at less than 10% level, suggesting some overreaction to extreme good news in F t . The disappearance of significance in Table 2 indicates that the overreaction effect for F t is not robust to sampling variations.

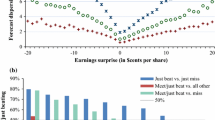

Graphically, after the effects on forecast optimism of high earnings uncertainty are taken away, the forecast error lines in Fig. 1 are lifted upward at both ends. At the high end, the downward slope for ΔEPS t−1 now becomes flat, and the flat slope for F t becomes steeper. At the low end, the upward slopes become less steep for ΔEPS t−1 and even downward for F t .

For the upper quarter of F t , the mean FE t is −1.33% and the mean DISP t is 3.56%. Thus, the average FE t after the uncertainty-induced bias is taken away is roughly −1.33% − (−0.34) × 3.56% = −0.12%.

Another possibility for the reversal of coefficient signs for the lower quartile is that DISP t is not linearly related to forecast errors. A linear specification may over or under-compensate the dispersion-caused bias when DISP t is high. This could affect the signs at the extremes of earnings levels due to the high correlation to DISP t (see Fig. 1). Barring a theory to functionally link forecast dispersions to forecast bias, it is not clear which functional form is appropriate. When we try the square root of, logarithm of, segmented, and squared DISP t , β L + β LL remains negative.

References

Abarbanell JS (1991) Do analysts’ earnings forecasts incorporate information in prior stock price changes? J Account Econ 14:147–165

Abarbanell JS, Bernard VL (1992) Tests of analysts’ overreaction/underreaction to earnings information as an explanation for anomalous stock price behavior. J Finance 47:183–198

Abarbanell JS, Lehavy R (2003) Biased forecasts or biased earnings? The role of reported earnings in explaining apparent bias and over/underreaction in analysts’ earnings forecasts. J Account Econ 36:105–146

Ahmed AS, Lobo GJ, and Zhang X (2000) Do analysts under-react to bad news and over-react to good news? Working paper, Syracuse University

Ali A, Klein A, Rosenfeld J (1992) Analysts’ use of information about permanent and transitory earnings components in forecasting annual EPS. Accoun Rev 67:183–198

Barberis N, Shleifer A, Vishny R (1998) A model of investor sentiment. J Financial Econ 49:307–343

Barron OE, Kim O, Lim SC, Stevens DE (1998) Using analysts’ forecasts to measure properties of analysts’ information environment. Account Rev 73:421–433

Basu S, Markov S (2004) Loss function assumptions in rational expectations tests on financial analysts’ earnings forecasts. J Account Econ 38:171–203

Brown LD (2001) A temporal analysis of earnings surprises: profits versus losses. J Account Res 39:221–241

Brown P, Foster G, Noreen E (1985) Security analyst multi-year earnings forecasts and the capital market. Studies in Accounting Research #21. American Accounting Association

Butler KC, Saraoglu H (1999) Improving analysts’ negative earnings forecasts. Financial Anal J 55:48–56

Brown LD, Han J (1992) The impact of annual earnings announcements on convergence of beliefs. Account Rev 67:862–875

Das S, Levine CB, Sivaramakrishnan K (1998) Earnings predictability and bias in analysts’ earnings forecasts. Account Rev 73:277–294

Daniel K, Hirshleifer D, Subrahmanyam A (1999) Investor psychology and security under- and overreactions. J Finance 53:1839–1885

DeBondt W, Thaler R (1990) Do security analyst overreact? Am Econ Rev 80:52–57

Diether KB, Malloy CJ, Scherbina A (2002) Differences of opinion and the cross-section of stock returns. J Finance 57:2113–2141

Eames M, Glover SM (2003) Earnings predictability and the direction of analysts’ earnings forecast errors. Account Rev 78:707–724

Elliott J, Philbrick D, Wiedman C (1995) Evidence from archival data on the relation between security analysts’ forecasts errors and prior forecast revisions. Contemp Account Res 11(2):919–938

Easterwood JC, Nutt SR (1999) Inefficiency in analysts’ earnings forecasts: systematic misreaction or systematic optimism? J Finance 54:1777–1797

Fan DK, So RW, Yeh JJ (2006) Analyst Earnings Forecasts for Publicly Traded Insurance Companies. Rev Quant Finance Account 26:105–136

Francis J, Philbrick D (1993) Analysts’ decisions as products of a multi-task environment. J Account Res 31:216–230

Gu Z, Chen T (2004) Analysts’ treatment of nonrecurring items in street earnings. J Account Econ 38:129–170

Gu Z, Wu JS (2003) Earnings skewness and analyst forecast bias. J Account Econ 35:5–29

Han BH, Manry D, Shaw W (2001) Improving the precision of analysts’ earnings forecasts by adjusting for predictable bias. Rev Quant Finance Account 17:81–98

Hayes RM (1998) The impact of trading commission incentives on analysts’ stock coverage decisions and earnings forecasts. J Account Res 36:299–320

Hayes RM, Levine CB (2000) An approach to adjusting analysts’ consensus forecasts for selection bias. Contemp Account Res 17:61–83

Hong H, Stein JC (1999) A unified theory of underreaction, momentum trading and overreaction in asset markets. J Finance 54:2143–2184

Kwon SS (2002) Financial analysts’ forecast accuracy and dispersion: high-tech versus low-tech stocks. Rev Quant Finance Account 19:65–91

Lim T (2001) Rationality and analysts’ forecast bias. J Finance 56:369–385

Machuga SM, Pfeiffer RJ Jr, Verma K (2002) Economic value added, future accounting earnings, and financial analysts’ earnings per share forecasts. Rev Quant Finance Account 18:59–73

McNichols, M, O’Brien P (1997) Self-selection and analyst coverage. J Account Res 35(Supplement), 167–199

Mendenhall R (1991) Evidence on the possible underweighting of earnings-related information. J Account Res 29:170–179

Mest DP, Plummer E (2003) Analysts’ Rationality and Forecast Bias: Evidence from Sales Forecasts. Rev Quant Finance Account 21:103–122

Ramnath S, Rock SK, Shane PB (2006) A review of research related to financial analysts’ forecasts and stock recommendations. Working paper, available at SSRN: http://ssrn.com/abstract=848248

Acknowledgments

Helpful comments by an anonymous referee, Mingyi Hung, Prem Jain and participants of the Chinese Accounting Professors Association Annual Meeting at Southwest University of Finance and Economics are gratefully acknowledged. We thank First Call for providing analyst forecast data.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Gu, Z., Xue, J. Do analysts overreact to extreme good news in earnings?. Rev Quant Finan Acc 29, 415–431 (2007). https://doi.org/10.1007/s11156-007-0037-8

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11156-007-0037-8